A decade ago, the price of gold was hovering around $1,150/oz.

Today, adjusted for inflation, that comes to about $1,500. Gold has more than kept pace with inflation over this period, but it puts the current landscape of gold miners in perspective.

Consider that today, the average all-in sustaining cost (AISC) for publicly traded companies is a touch over $1,500/oz. If you’re not familiar with AISC, it’s a relatively new development, created by the World Gold Council in 2013 to give a universal benchmark for discussing how much it costs to mine an ounce of gold.

Before 2013, gold miners used all kinds of metrics and accounting gimmicks to report how much it cost them to mine. Some of them were useful. Many of them were confusing or misleading. It was extremely difficult for most investors to make an apples to apples comparison between companies because there was no unified standard.

Is the AISC perfect? No, but at least it’s a single, agreed upon metric that gives you a more accurate way to compare different companies.

One major issue with the AISC is that it’s not static. It’s a snapshot. It changes because most of its inputs are not set in stone: they’re highly susceptible to inflation and other dynamic factors. Consider that the price of fuel, equipment, labor, taxes, financing, permitting et al are always moving – and most of them are sensitive to inflation.

In fact, as much as gold is responsive to inflation, there’s no guarantee that it will outpace or even keep pace with a company’s AISC…

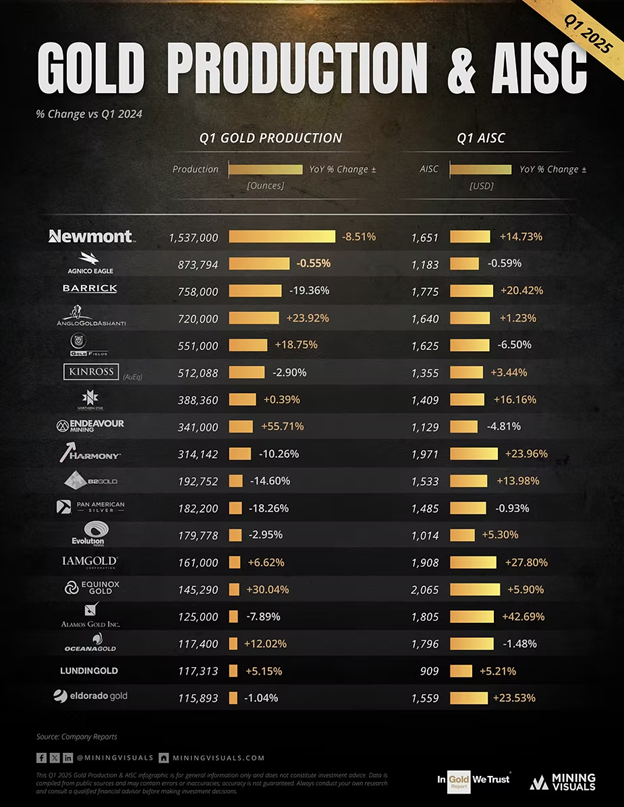

Just look at this chart from Mining Visuals, showing the growth of AISC for gold majors between Q1 2024 and Q1 2025:

Some of these companies saw their costs rise almost as much as gold did over the same period. Remember, gold rose about 30% between Q1 2024 and Q1 2025. That means if a company’s costs rose similarly, they can mine as much as they want but their profits will stay the same. If they’re diluting shareholders or taking on debt to do it, they’re not just treading water, they’re sinking.

You’ll even notice a kind of trend in this chart: companies that saw their AISC fall tended to mine more. Companies that saw their costs rise tended to mine less. No surprises there.

This past year has been kind of an anomaly. Gold actually has outpaced AISC for the most part. That means most gold miners can mine at a bigger profit…

But that’s not typically how it works. Usually, AISC and gold are not far off from each other. Which means gold majors are on a very difficult treadmill – always in danger of dipping into the red if anything goes wrong.

If you were starting to build a mine 10 years ago (which is about how long it takes to build after you are done drilling and exploring a deposit), that means you probably wouldn’t be interested in developing a mine that had a potential AISC much over $1,100/oz.

You would be setting yourself up to lose money on every ounce mined – or you would be making a huge bet that gold prices would rise much higher.

Finding an economic gold deposit a decade ago meant you really had to get under $1,000/oz AISC…

But that’s extremely difficult. Anything close to $1,000/oz AISC with over 500,000 ounces is considered a world class, tier 1 mine.

There just aren’t that many mines like that out there.

In fact, the only ones that I know of are in my portfolio right now.

And if you’re thinking that $4k/oz gold might be changing this picture, you’re probably right. What’s going to happen is that we will see lots of juniors pop up like mushrooms after a rainstorm. Most of them will not be wise investments – because they’ll be baking in $4k gold to their business plan.

Meanwhile, we still have a chance to own companies that built or are still in the process of building mines with $1,500 gold in mind. Those are the companies you want to own today.

Best,

Garrett Goggin, CFA, CMT

Lead Analyst and Founder, Golden Portfolio